Real estate market overview

Real estate market overview rents and prices

Thomas & Simonova

Over the last years, a large number of new, interesting residential projects with modern architecture and energy-efficient solutions have arisen in Ukraine. The residential complex ceases to be just a place where people come to spend the night. The concept of new projects is to create property that enhance quality of life for a single family unit. The design of the apartment and the leisure services provided for residents are being planned out in advance and the number of services and their quality is increasing. The market still has some issues to work out: both in terms of implementation of modern facilities and services and in terms of the quality of construction work and structural solutions of buildings. However, the market is entering a new stage of development, when the speed of developers’ response to consumer preferences increases significantly and determines the competitiveness of the project.

In April 2018, apartments were offered for sale by 78 developers in 208 developments . These include both unfinished construction projects and unsold apartments in buildings that have been put into operation.

Development and offer of new buildings in the primary market in Kyiv as of selected dates

In April 2018, the price per square meter of apartments in 15 new buildings increased by 500-2,000 UAH/sq.m. However, the price in 12 other buildings decreased by 500-1,000 UAH/sq.m.

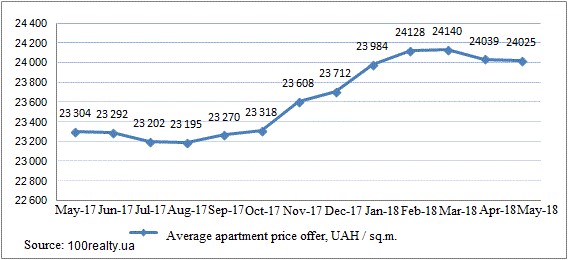

In April 2018, the average price of apartments in the 208 new buildings shown above in Kyiv was 24,039 UAH/sq.m. Over the past year (April 2017 to 2018), the average price of 1 sq.m of apartment space in new buildings in Kyiv increased by 3.3%, although there was a slight decline from March to April 2018.

Trend in the average price for apartments in new buildings in Kyiv

Average prices for apartments in new buildings in the districts of Kyiv, April 2018

Over the period March to April 2018, the change in prices for new-built property, by property class, is shown below:

- economy class – decrease by 0.6% to 18,009 UAH/sq.m

- comfort class – increase by 0.6% to 22,193 UAH/sq.m

- business class – increase by 0.2% to 32,448 UAH/sq.m

- premium class – increase by 0.3% to 50,489 UAH/sq.m

Average price of apartments in new buildings in Kyiv by class and number of rooms, April 2018.

|

Class |

Quantity of Residential Complexes / rooms |

Selection of apartments, units |

Average total area, sq. m |

Average price of an apartment, UAH |

Average price, UAH/sq. m |

|

Total in Kyiv |

208 |

2 049 |

72 |

1 795 781 |

24 039 |

|

Economy |

56 |

797 |

67 |

1 212 210 |

18 009 |

|

one-room apartment |

258 |

42 |

804 246 |

18 359 |

|

|

two-room apartment |

310 |

66 |

1 208 927 |

18 020 |

|

|

three-room apartment |

188 |

89 |

1 573 018 |

17 702 |

|

|

four-room apartment |

41 |

125 |

2 149 780 |

17 124 |

|

|

Comfort |

77 |

776 |

69 |

1 520 983 |

22 193 |

|

one-room apartment |

265 |

41 |

949 095 |

22 635 |

|

|

two-room apartment |

267 |

67 |

1 465 588 |

21 932 |

|

|

three-room apartment |

183 |

91 |

1 971 719 |

21 893 |

|

|

four-room apartment |

61 |

139 |

2 895 679 |

22 317 |

|

|

Business |

49 |

352 |

83 |

2 702 884 |

32 448 |

|

one-room apartment |

114 |

50 |

1 685 362 |

33 733 |

|

|

two-room apartment |

105 |

76 |

2 335 056 |

30 657 |

|

|

three-room apartment |

101 |

106 |

3 475 238 |

32 489 |

|

|

four-room apartment |

32 |

154 |

5 097 001 |

33 615 |

|

|

Premium |

26 |

124 |

93 |

4 691 339 |

50 489 |

|

one-room apartment |

42 |

58 |

2 853 020 |

49 865 |

|

|

two-room apartment |

34 |

83 |

4 273 440 |

50 968 |

|

|

three-room apartment |

35 |

118 |

5 924 951 |

49 919 |

|

|

four-room apartment |

13 |

160 |

8 402 230 |

52 783 |

Today apartments are offered for sale that will be completed in 2019-2020. There is no obvious oversupply of apartments on the market now or looking out over the next few years. The balance between new developments and market demand has been better managed by developers in recent years.

The offer of new apartments in 2017 continued to grow at a record pace – sales were opened in 59 new residential projects and 45 projects under construction put into sale new stages of their complexes. The total number of apartments in new complexes and stages was more than 55 thousand apartments. At the end of December 2017, 73 developments were at the final stages of sales (less than 10% of apartments were left for sale).

In 2017, the structure of new offers underwent significant changes: the share of the economy class complexes decreased sharply to 21%, compared to 59.5% in 2016. The comfort class complexes increased to 45%, in comparison with 27% in 2016. The share of the business class complexes has increased more than twice – up to 30%, compared to 13.5% a year earlier. In 2017, a positive trend was also shown by the premium segment – the share of new offers in this class was 4%.

The leaders in terms of the volume of the new offer in 2017 were Shevchenkivskyi and Holosiivskyi districts (21% and 20%, respectively). Compared to 2016, the share of Pecherskyi district in the structure of new offers increased significantly: it was 16% against 6% in the previous period. In fact, in these three districts more than half of the new complexes are concentrated. In Darnytskyi and Solomyanskyi districts, sales were opened in 6 complexes in each.

Quality of development has continued to increase, with 45% of new apartments being in the comfort class complexes. The average price for a square meter in the capital’s new buildings increased in 2017 by 11.6%. The largest increase in prices was registered in the business class complexes – the prices increased by 36.4% compared to December 2016.

The structure of new offers for the number of rooms has shifted slightly towards two-room apartments, but the main share in new offers is still one-room apartments – 47%, and two-room apartments – 32%. The share of three-room apartments in the structure of new offers is 17%.

DEMAND

The main trend in demand for newly-built residential property was an increase in investor interest in prestigious housing – new complexes of the business and premium classes. Relative to 2016, demand for business class housing increased by 15% during the first half of 2017 and by 21% by year’s end. The demand for premium housing increased by 2% YOY. Nevertheless, demand is mainly concentrated in the budget segment. Economy class apartments represented 53% of total demand during 2017. Demand for the comfort class category of apartments declined 24% during 2017 reflecting a more balanced and informed approach by buyers to the choice of apartments and the evaluation of residential complexes: with generally identical building and apartment characteristics, prices in the comfort class complexes were 30% higher on offer than in the economy class complexes.

At the end of 2017, demand for business class apartments reached 21% in the total demand structure.

On average for the year, aggregate sales in new buildings in Kyiv in 2017 ranged from 1,000 to 1,350 apartments per month. The highest rates were typical for new residential complexes at the start of sales, where apartments were offered at a low price with a long installment plan. In some residential complexes, monthly sales rates reached 50-70 apartments per month.

PRICE DEVELOPMENT

In 2017, prices in most classes showed a relatively stable upward trend. Prices for the economy class housing grew gradually throughout the year (a slight decrease was noted only in the summer period). The growth in prices in the economy segment for 12 months was 11.3%. Slightly greater volatility during the year was shown by prices in the residential comfort class complexes – after a slight increase in the first quarter, the price development in the segment acquired a downward trend, followed by a slight increase in the fourth quarter. At the end of the year, the comfort class prices increased by 1.5%.

Since the beginning of the year, prices in the business class complexes have grown steadily – some correction occurred by the end of the third quarter, but by the end of the year, the growth in prices for the business class housing was a record-breaking 36.4%.

The price development in the premium segment was characterized by jumps in prices; prices were significantly reduced twice in the year (in March and September), however, by the end of the year, average prices in the premium class returned to the level of December 2016 – the price decrease was only 0.6%.

Average prices in the newly-built residential property market grew in 8 districts out of 10. The largest growth was registered in Pecherskyi, Darnytskyi, Holosiivskyi and Obolonskyi districts, where a significant part of the complexes are in the late stages of development, which led to an increase in average prices between 16.7% to 22.5%. Average prices per square meter in Svyatoshynskyi district increased by 10.3%, in Dniprovskyi district by 4.3%, and in Desnyanskyi district by 2.6%.

Average price declined by 12.2% in the Solomyanskyi district reflecting increased competition caused by the construction of a large number of new complexes in the budget segment in 2016-2017. The largest drop in average price was registered in Shevchenkivskyi district and amounted to 14%. The main reason was the opening of sales in several very large projects such as the Residential Complex “Faina Town”, the Residential Complex “Baggoutovskyi” and the Residential Complex “Henesi House”, where prices were much lower than the mid-market prices for that class of developments.

FORECAST

In 2018, further replenishment of the market with new residential facilities is expected, while the main source of offer replenishment is likely to be new stages of existing residential complexes. An unstable exchange rate of the national currency and increases in the cost of construction materials and labor rates will continue to put pressure on the lower price limit for budget segment complexes, which will lead to further price increases in the economy and comfort classes. Demand is expected to increase up to 10%, but not more. The hryvnia prices in 2018 are most likely to have multidirectional development depending on the class and district of the complex. Against the background of a total increase in average prices, a correction in price for a square meter in the complexes of the prestigious segment in the first half of 2018 is possible.

In the absence of significant currency exchange rate fluctuations, overall demand for new apartments will remain at the level of 2017, although there is a high probability of reorientation of some buyers to the secondary housing market, where investment apartments are offered in new buildings brought into service. The importance of non-price competitive advantages of residential complexes will continue to grow: projects where higher quality infrastructure and various new services and facilities and energy-efficient “things” are implemented on time and in full will be in high demand.

CONCLUSIONS

In Ukraine, the demand for comfortable, quality housing with more modern infrastructure and amenities is growing.

The number of new residential complexes is growing and expected to continue.

Demand and prices within the premium segment continue to grow and most apartments are sold during the initial stages of construction.

The market overall continues to be concentrated in the economy and comfort sections of the market reflecting the general level of income and associated demand by the general population. Average prices are expected to grow but with demand shifting over time to a preference for economy versus comfort sections, a possible continuation of price corrections in the latter may occur.

This market summary has drawn on a number of reputable, publically available sources and been augmented by the appraisers personal experience.